Key Takeaways

Ethereum accomplished its long-awaited Merge improve in September 2022

Stakers are at the moment incomes roughly 4% APY from their Ether tokens

19% of the full Ether provide is staked, the bottom ratio of any of the main cash

Staking rewards are divided amongst stakers, that means the APY earned decreases as extra customers stake

Demand on the community will increase gasoline charges and in the end contributes to extra APY, that means there are a number of components at play when attempting to evaluate the place the yield could land

All in all, it stays up for debate as to the place the yield is headed, regardless of many analysts predicting basement-level yields of 1%-2% are inevitable

The basics of Ethereum had been totally remodeled in September 2022 when the Merge went stay, the blockchain formally turning into a proof-of-stake consensus. The implications for this are many, nevertheless one of many extra fascinating points is that traders can now earn a yield from staking their Ether tokens.

Let’s dive into how standard staking has been, the place it’s trending going ahead, and speculate about the place the all-important APY could land.

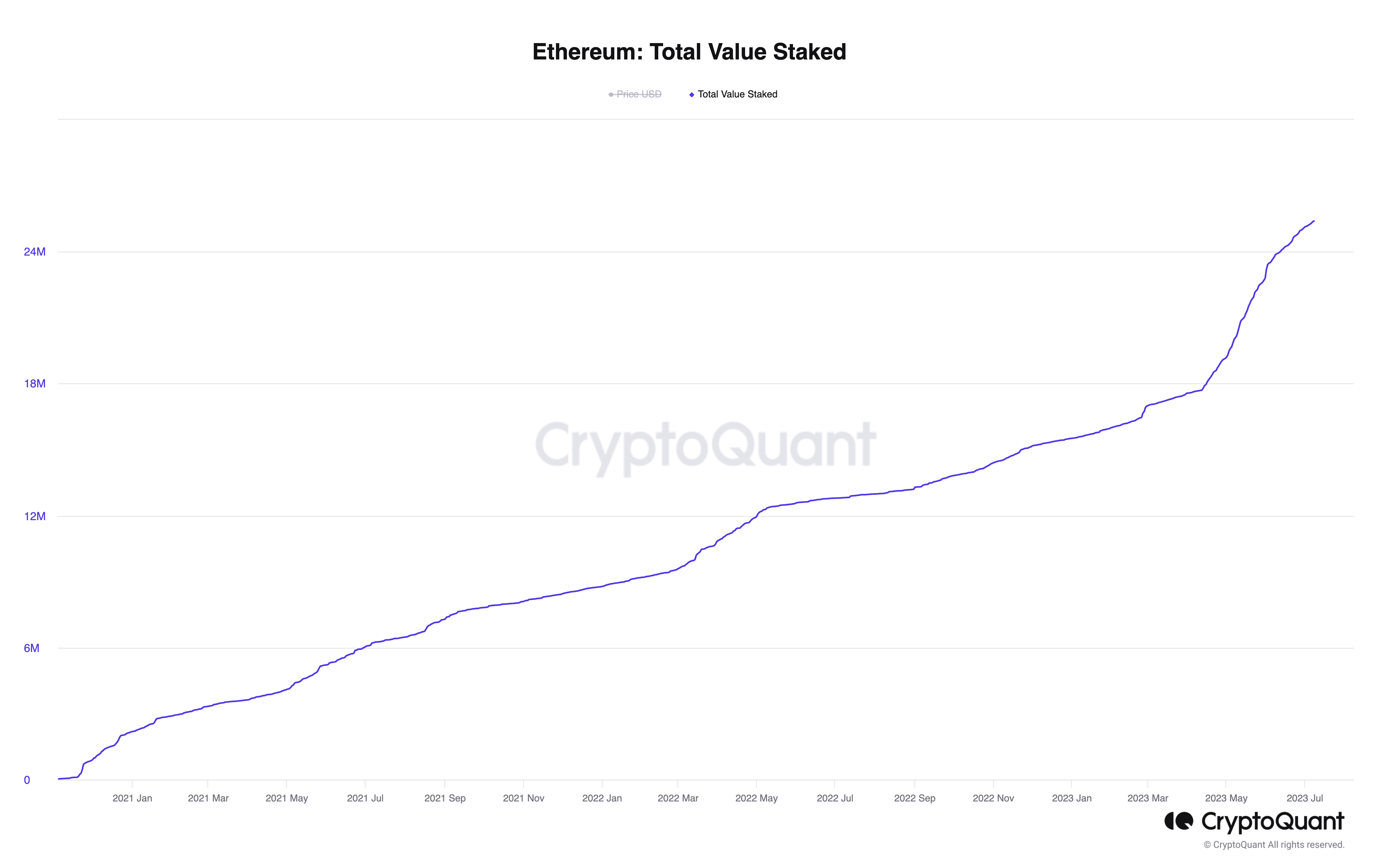

Ethereum stakers are growing

Ethereum staking has proved wildly standard. There’s at the moment nearly 18.75% of the full provide staked. The under chart from CryptoQuant reveals that not solely has the rise been constant, however the charge of improve has steepened noticeably because the Shapella improve in April.

Shapella lastly allowed staked Ether to be withdrawn, with some early stakers having had tokens locked up since This autumn of 2020. There was therefore some concern that Ether could be withdrawn en masse as soon as the Shapella improve went stay, the following promote strain certain to dent the value. Not solely has this occurred, however staking has solely grow to be extra standard because the improve.

Regardless of the recognition of Ethereum staking, and the dearth of withdrawals sparked by Shapella, the community’s staked tokens as a % of the full provide nonetheless pale compared to different proof-of-stake blockchains.

Regardless of the recognition of Ethereum staking, and the dearth of withdrawals sparked by Shapella, the community’s staked tokens as a % of the full provide nonetheless pale compared to different proof-of-stake blockchains.

The chart under highlights Ethereum in yellow, its 19% ratio far under the opposite main proof-of-stake cash. Assessing the remainder of the highest 10 by staked market cap, these cash common a 53% stake ratio, with solely BNB Chain remotely near Ethereum, sitting at 15%.

If we then shift the chart to evaluate the full market cap of the staked portion of cash, Ethereum’s dominance is obvious. Its 19% staked tokens carry a worth of $43 billion – greater than the opposite 9 cryptos’ staked market caps mixed.

Ethereum’s low staked ratio implies that it ought to have extra, at the very least if different cash can be utilized as a benchmark. That is very true when contemplating latest bullish developments on the Ethereum community which recommend it could be solidifying its place because the market-leading good contract platform. Most notable of those might be dialogue round potential Ether futures ETFs, in addition to the announcement that PayPal is launching a stablecoin on the community this week.

So, what occurs to the staking yield if the quantity of staked Ether does certainly proceed to extend? Bear in mind, the full annual yield paid out to stakers is calculated as follows:

[(gross annual ETH issuance + annual fees*(1-% of fees burned)]

These complete staking rewards are then divided by the common ETH staked over the yr to commute the APY.

In different phrases: The quantity of ether staked is within the denominator of the fraction. In order the quantity staked will get greater, the APY shrinks. This impact can already be seen in what has occurred so far. Analysts had predicted a yield of 10%-12% forward of the Merge, nevertheless at the moment it’s nearer to 4%. And that’s 4% with its staking ratio fully out of whack in comparison with different proof-of-stake cash, as talked about above.

What occurs subsequent?

With the quantity of Ether staked growing incessantly, is the yield due to this fact primed to break down?

Some analysts consider it’s headed in direction of 1%-2%; some even assume much less. The fact is that no person actually is aware of as a result of, as all the time, demand depends on a wide range of components.

We have to bear in mind, as we regularly say in these columns, that speculating on the way forward for crypto is so troublesome as a result of now we have such little information to work with. That is true for Ethereum as a complete, which solely launched in 2015, however particularly so concerning the yield, because the Merge has solely been stay since September (or since April in the event you rely the “true” completion date as post-Shapella).

Therefore, it’s a problem to forecast the staking yield going ahead. We’ve got targeted on the spectacular development of staking to this point, and whereas it will drive the yield down, demand on the community will improve the numerator of the aforementioned method and kick the yield up.

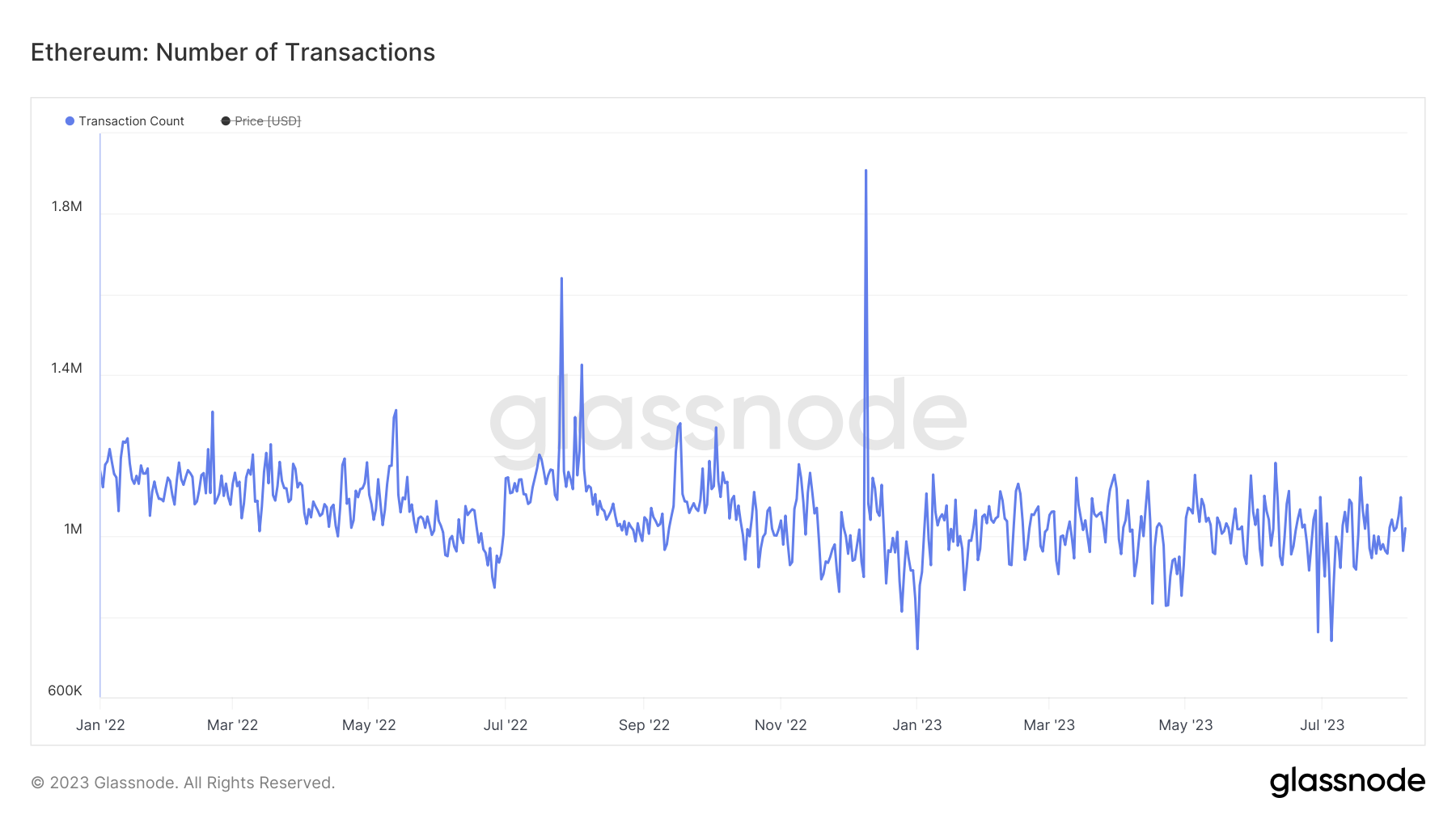

Certainly, complete transactions, the speed has been fairly resilient all through the final eighteen months, regardless of the massacre within the sector final yr.

Then once more, crypto is altering rapidly. It stays troublesome to foresee how regulation, infrastructural improvement (restaking and Eigeanlayer spring to thoughts for example) and the macro panorama, simply to call just a few components, will have an effect on the local weather going ahead.

Talking of macro, there may be additionally the matter of trad-fi yields. At the moment, the Fed funds charge is 5.25%-5.5%, having been near-zero previous to March 2022. Backing out chances from Fed futures implies the market is anticipating the tip of the cycle is close to. To not point out, with the mammoth quantity of debt within the present system, charges can’t keep excessive without end.

Might falling trad-fi yields have an effect on demand for staking yield? Maybe – whereas it’s exhausting to separate the general liquidity drain and suppressing of threat property that happens out of hiked charges, the superior (and risk-free) return is certainly a key cause why capital has flooded out of DeFi within the final yr. Whereas previously-dizzying DeFi yields have collapsed, trad-fi yields have rocketed because the Federal Reserve has scrambled to rein in rampant inflation.

Moreover, if yield does fall down in direction of 1%-2%, stakers might start to drag out and search elsewhere for revenue. This may due to this fact create a reflexive relationship with regard to the yield.

All in all, it stays too early to take a position about the place the Ethereum staking yield is in the end headed, at the very least with any diploma of confidence; it depends upon too many components and the pattern area is simply too temporary so far. It does appear seemingly, if not inevitable, that the yield will decline to some extent, however the query of how a lot is a troublesome one to reply. Whereas many are adamant the APY will cascade downwards to uber-thin ranges – and for the avoidance of doubt, it could do – now we have introduced right here at the very least some factors of consideration as to why the scenario will not be as clear lower.

{kind=link}