Initially printed on Unchained.com.Unchained is the official US Collaborative Custody companion of Bitcoin Journal and an integral sponsor of associated content material printed by Bitcoin Journal. For extra info on companies provided, custody merchandise, and the connection between Unchained and Bitcoin Journal, please go to our web site.

You don’t usually see the time period “Roth IRA” trending on-line, however in 2021, tech investor Peter Thiel made headlines for his $5 billion tax-free Roth IRA piggy financial institution. How did he do it? The reply is various investments. He used a self-directed IRA to put money into early-stage tech corporations a number of instances over. Is it a loophole? Probably. Nevertheless it occurred, it acquired consideration, and the IRA construction in query may come beneath additional scrutiny.

“Thiel has taken a retirement account value lower than $2,000 in 1999 and spun it right into a $5 billion windfall.” – ProPublica (2021)

Let’s have a look at six frequent dangers related to self-directed and checkbook IRAs, how they could apply within the context of bitcoin, and why there could also be elevated regulation coming sooner or later. However first, we have to outline our phrases and differentiate between IRA constructions.

The totally different IRA constructions

The totally different IRA constructions can behave in an “each sq. is a rectangle, however not all rectangles are squares” form of approach. IRAs will be Conventional (pre-tax) or Roth (post-tax) no matter custodial relationship/construction. All IRAs are custodial. A custodian, within the context of IRAs, is a licensed monetary establishment overseeing and administering the IRA.

Brokerage and Financial institution IRAs

Brokerage and financial institution IRAs are essentially the most acquainted and customary sorts. Brokerage and Financial institution IRAs permit buyers to put money into shares, bonds, ETFs, mutual funds, and different securities, in addition to banking merchandise (CDs, deposit accounts, and so forth.). Examples embrace your typical Constancy, TD Ameritrade, or Charles Schwab IRA. The Unchained IRA is closest to this construction on this hierarchy.

Self-directed IRA (SDIRA)

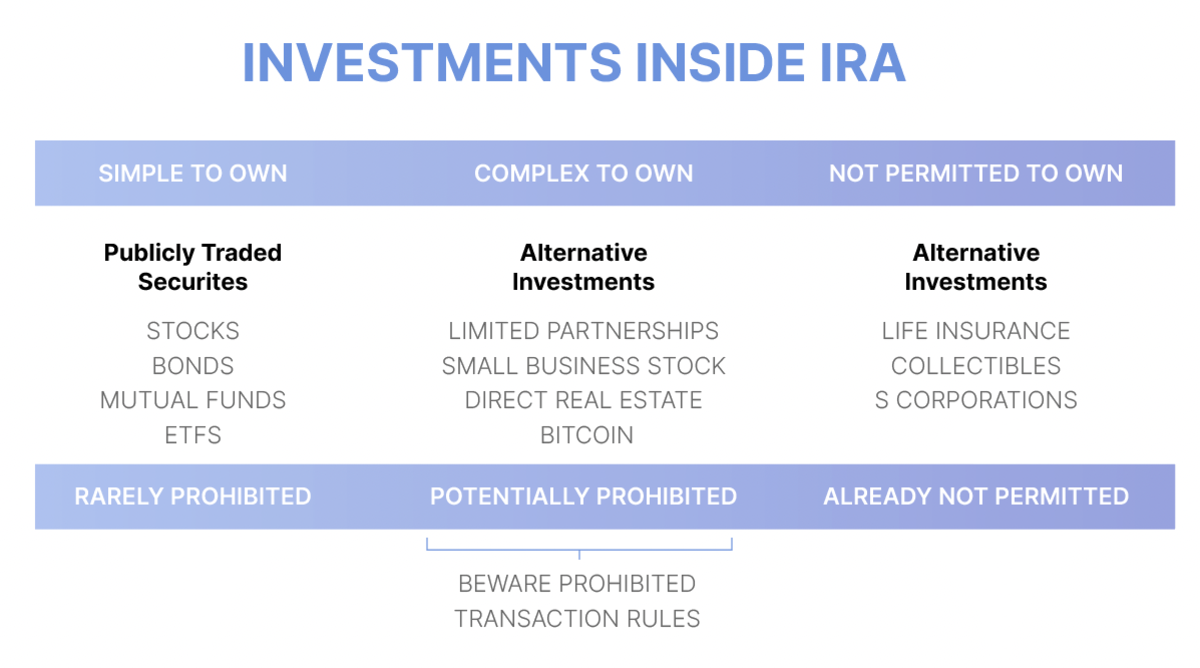

A self-directed IRA is a custodial IRA the place the custodian permits for expanded funding choices outdoors of or along with typical brokerage and financial institution belongings (shares, bonds, CDs, and so forth.). House owners of self-directed IRAs can put money into non-traditional belongings like actual property, companies, non-public loans, tax liens, treasured metals, and digital belongings. Though the IRS doesn’t have a definitive listing of allowed investments, it definitely has a number of that aren’t allowed (collectibles, life insurance coverage, sure derivatives, S-Corps, and so forth.).

Checkbook IRA

Checkbook IRAs are a subset of self-directed IRAs. The time period “checkbook IRA” isn’t customary, but it surely often refers to a self-directed IRA that offers an account proprietor management of investments by a checking account, often by an LLC conduit. The account holder can then make investments with IRA funds just by writing a test (“checkbook management”). With the added freedom of extra funding selections comes added duty of administration, in addition to authorized ambiguity as as to if the construction nonetheless qualifies as a tax-exempt IRA.

Non-checkbook self-directed IRA

A subset of self-directed IRA the place the custodian approves transactions earlier than investments are made. Buyers should look forward to the custodian to evaluate every potential funding and formally settle for title to the underlying asset. These had been generally used for actual property and personal fairness investments and started regaining reputation as soon as extra authorized uncertainties arose relating to checkbook IRAs in late 2021 (mentioned in part 4 under).

Dangers to observe for when utilizing a self-directed or checkbook IRA

1. Liquidity

Sadly, many self-directed belongings lack liquidity, making them troublesome to promote shortly. Examples embrace actual property, privately held companies, treasured metals, and so forth. If money is ever wanted for a distribution or inner expense, promoting an asset quick might be an issue (which compounds into different issues, i.e., by accident commingling funds). Self-directed IRA homeowners ought to conduct thorough due diligence on asset liquidity earlier than committing to an funding technique.

2. Formation and authorized construction

When forming a checkbook IRA, a self-directed IRA LLC is established first. Then, the LLC establishes a checking account identical to another enterprise entity. Subsequent, the LLC is funded by sending the IRA funds to the checking account.

With the right authorized construction, the IRA proprietor can turn out to be the only real managing member of the LLC and have signing authority over the checking account. Nevertheless, improper authorized construction, registration, or titling may all trigger severe issues for the tax-advantaged standing of the IRA. Many checkbook IRA facilitators are competent, however errors may all the time result in points and attainable disqualification/lack of your complete IRA.

3. Misreporting transactions

Inside a checkbook IRA, homeowners can fund investments shortly and freely, however this comes with the duty of correctly following guidelines and self-reporting transactions.

On the finish of every 12 months, the proprietor of the LLC might want to present full transaction particulars to its IRA custodian and submit honest market valuation (FMV) info. With out oversight into every transaction you make, a custodian is extra more likely to misreport earnings in your investments. All the time make sure the custodian has correct info to keep away from by accident breaking the regulation.

4. “Deemed distribution” therapy

Shoppers trying to purchase treasured metals, actual property, or digital belongings ought to know the danger of “deemed distributions” therapy. A latest United States tax courtroom case, McNulty v. Commissioner, illustrates the appreciable dangers of sustaining a checkbook IRA. Within the McNulty case, a taxpayer used her checkbook IRA LLC to buy gold from a treasured metals vendor. She saved the LLC’s gold at dwelling in her private protected. The courtroom dominated that her “unfettered management” over the LLC’s gold with out third social gathering supervision created a deemed taxable distribution from her IRA.

It’s unattainable to understand how far a tax courtroom will go making use of “deemed distribution” therapy to any given transaction or funding inside a checkbook IRA. For checkbook IRA homeowners that maintain the keys to bitcoin in an unsupervised construction, there’s a threat that the McNulty ruling may trigger your whole IRA to be topic to tax. Additional, since various investments had been pretty lately (2015) added to IRS Publication 590, it’s totally attainable that the IRS and Congress may apply extra scrutiny to checkbook IRAs going ahead. Learn extra in regards to the McNulty case and its implications.

5. Prohibited transactions

All self-directed IRA homeowners are all the time prohibited from commingling private and IRA belongings or utilizing any private funds to enhance IRA belongings. “Self-dealing” is among the commonest pitfalls for self-directed account holders. For instance, in case you use your IRA to buy actual property, you aren’t allowed to make use of the property your self—not even a bit bit. You can not dwell there, keep there, or hire workplace house to your self there. You aren’t even allowed to make your individual repairs or present “sweat fairness.”

It’s not solely the IRA proprietor that may’t take part in any “self-dealing,” however spouses, youngsters, and grandchildren as effectively. They’re thought of disqualified people, and penalties are stiff. These are stringent guidelines and may end up in large tax complications if breached. I don’t intend to crush any goals, however investing your 401k/IRA into your lakefront Airbnb trip dwelling and having you or your loved ones keep there even as soon as is a nasty concept. No buying a rental dwelling and renting it out to members of the family both. For additional enjoyable, see the IRS listing of prohibited transactions right here.

Listed here are a number of examples of how prohibited transactions guidelines might be utilized to digital asset buyers:

Commingling private wallets with IRA walletsLeverage with no non-recourse loanInvesting in sure collectible NFTs1

6. Financing

Financing inside a self-directed IRA can be extra difficult for a number of causes:

Usually, a non-recourse mortgage and bigger down fee are wanted for any property purchases.Sudden prices and charges can add up shortly and eat into any income.IRA-owned energetic companies may run into the difficulty of UBIT (Unrelated Enterprise Revenue Tax). This additionally impacts the overlap of bitcoin mining inside an IRA.Any earnings and bills should stay inside the IRA construction and by no means commingled with private funds. For instance, when the water heater goes out (actual property) or salaries must be paid (companies), the IRA itself should pay for these companies out of the IRA’s personal money. IRA homeowners might be tempted to co-mingle funds briefly as they search for short-term liquidity to unravel their money wants.

What does this imply for bitcoin IRAs?

The self-directed IRA house has many potential dangers if not correctly managed. The IRS and Congress have been paying particular consideration to how these constructions are used and abused. Mix this with their curiosity in regulating digital belongings, and the panorama seems ripe for additional scrutiny. With that, bitcoin IRAs want a singular strategy that mitigates these pitfalls.

Unchained IRA isn’t a checkbook IRA

Should you’re trying to maintain precise bitcoin in your IRA account, it is best to take into account the Unchained IRA. It’s not a “checkbook IRA” the place transactions have to be self-reported, and Unchained makes use of its key within the collaborative custody setup to trace inflows and outflows of IRA vaults. That visibility mechanism permits the custodian to actively monitor the IRA and subsequently permits customers to stay compliant with present IRA guidelines and rules.

There isn’t a self-reporting required, and the non-checkbook construction helps mitigate the danger of potential pitfalls (McNulty, misreporting transactions, and so forth.). If bitcoin appreciates like many buyers hope and anticipate, holding cash in an IRA construction correctly is of the utmost significance.

This text is supplied for academic functions solely, and can’t be relied upon as tax recommendation. Unchained makes no representations relating to the tax penalties of any construction described herein, and all such questions must be directed to an lawyer or CPA of your alternative. Jessy Gilger was an Unchained worker on the time this put up was written, however he now works for Unchained’s affiliate firm, Sound Advisory.

1While not technically a part of the Prohibited Transaction Guidelines (part 4975 of the Inside Income Code), collectibles are individually prohibited from being held in an IRA beneath part 408(m).

Initially printed on Unchained.com.Unchained is the official US Collaborative Custody companion of Bitcoin Journal and an integral sponsor of associated content material printed by Bitcoin Journal. For extra info on companies provided, custody merchandise, and the connection between Unchained and Bitcoin Journal, please go to our web site.

{kind=link}