Smart and Revolut have been leaders within the fintech cross-border transactions house, disrupting conventional banking programs. With Revolut’s IPO probably coming in 2025, it’s fascinating to match each firms to find out whether or not Smart is positioned to problem Revolut’s dominance or if the 2 serve totally different functions for traders.

Key Highlights

Smart trades at a fraction of Revolut’s personal valuation.

Smart Nearing All-Time Highs, however nonetheless not costly.

Banks are positioning within the battle to come back: Smart offers.

Seeing Revolut In all places

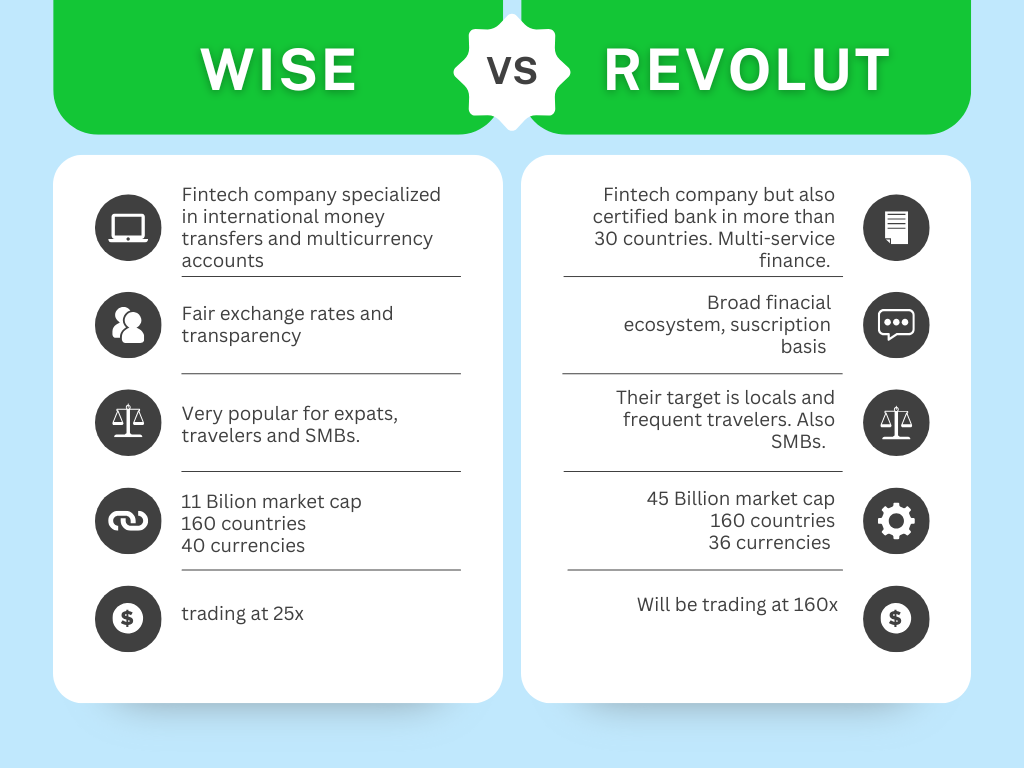

Throughout a current journey to Spain, I couldn’t escape Revolut’s advertisements. Aggressive advertising and IPO rumors acquired me pondering: How will a publicly traded Revolut have an effect on Smart? Whereas each are fintech firms, and disruptors to conventional banking, their methods and enterprise fashions differ considerably.

Smart’s mission is evident: low-cost, clear, and environment friendly cross-border transfers. Revolut, then again, goals to change into a world monetary super-app, providing the whole lot from banking to crypto. Given these distinct targets, ought to traders actually be evaluating the 2?

Revolut’s IPO particulars are nonetheless scarce, however a secondary share sale occurred in August 2024, factors towards a $45 billion valuation. That’s a large valuation, particularly for an organization that, whereas rising quick, hasn’t constantly been worthwhile. In the meantime, Smart is buying and selling at 25x P/E with regular profitability and a powerful return on capital. Let’s take a more in-depth have a look at their enterprise fashions.

Companies Mannequin Breakdown: Smart vs. Revolut

Smart is without doubt one of the world’s quickest rising fintech, whereas being very worthwhile. Launched in 2011, the enterprise is listed on the London Inventory Trade below the ticker, WISE. In fiscal yr 2024, Smart supported round 12.8 million individuals and companies, processing roughly £118.5 billion in cross-border transactions, and saving prospects over £1.8 billion, in line with the data offered by the corporate.

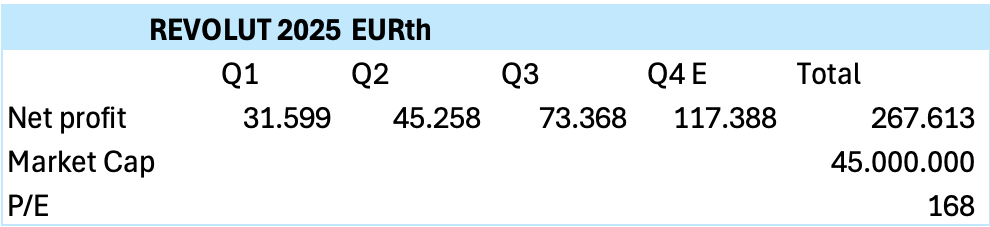

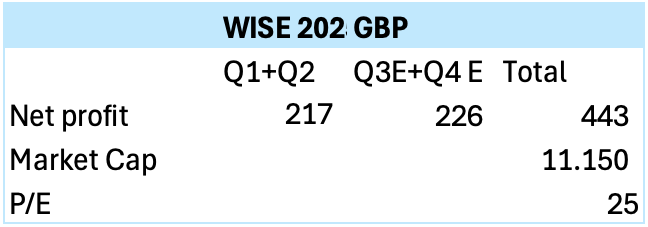

The true valuation of Revolut’s IPO continues to be unsure, though the obtainable info factors to a $45Bn worth, given current transactions. For the reason that final annual assertion obtainable for Revolut on their web site is dated for 2023 and the newest monetary report was with date 30 of September 2024, I needed to make some common predictions to match each firms:

1 GBP in hundreds of thousands

2 EUR, in 1000’s

As a reference, Revolut’s valuation could be nearly 7 occasions Smart’s present valuation. This implies two issues, doubtlessly: Smart is undervalued and Revolut is overvalued. For my part, each are appropriate, and I wouldn’t put money into Revolut given the newest identified valuation.

Smart, buying and selling at 25x P/E, is an fascinating alternative, rising 15-20% yearly. With stable returns on capital employed since 2018, proving the administration dedication in price discount and improve the shareholder’s revenue.

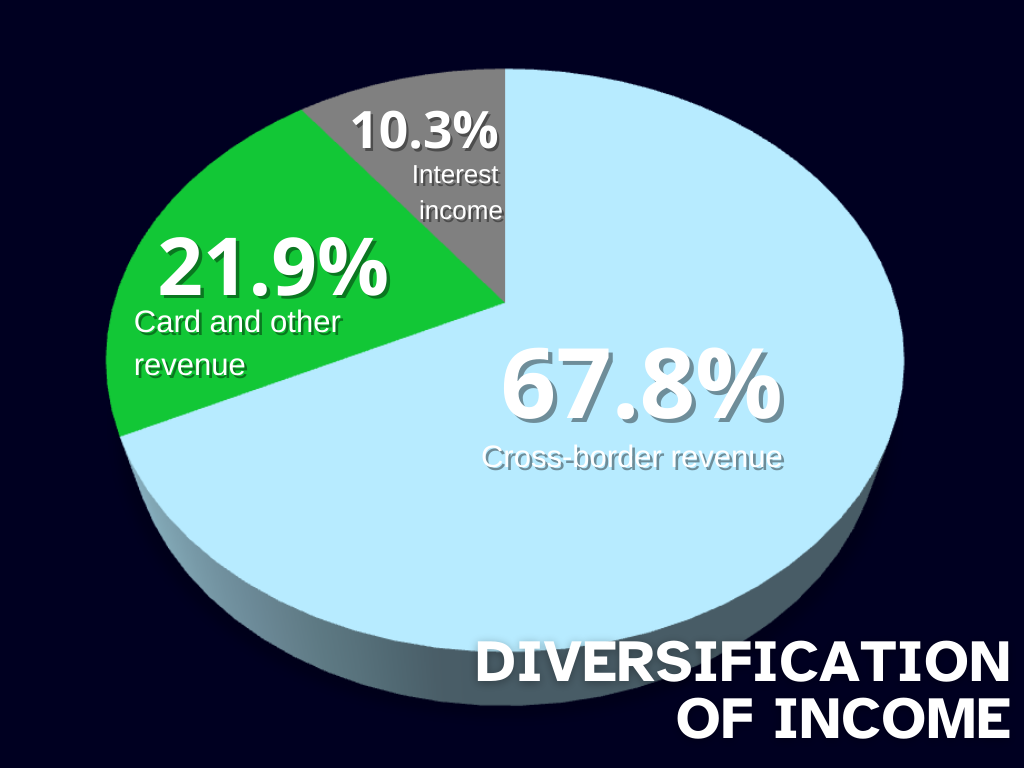

Smart is a Fintech (used to explain new know-how that seeks to enhance and automate the supply and use of monetary providers). Utilizing Smart’s platform, prospects can transfer their cash overseas to 40 totally different currencies in just one account. The corporate primarily generates income from cash transfers, conversion providers and debit card providers. Smart additionally generates income from its multi-currency funding function. This function permits prospects to buy items in funding funds, offered by fund managers, utilizing their Smart account stability.

The client development fee has been of 29% in 2024 in contrast with 2023, even thought, they needed to pause sensible enterprise new accounts as a result of they’re rising too quick for his or her capability! This yr they’re centered on put money into infrastructure to get the flexibility to produce the large current demand.

The final a part of the income that’s essential to spotlight is the curiosity revenue with a ten.3% of the income with a worth of 120.7m (this income solely considers the curiosity revenue of the primary 1% yield. If we think about all of the curiosity revenue, below and over 1%, it could be 485m). That is comprised of investments in cash market funds, listed bonds, and curiosity from money at banks.

To create a clear and real looking solution to transfer your cash overseas, they think about the mid-market change charges which is the worth the banks are prepared to pay for getting or promoting the currencies, and the mid-point between each is the mid-market change fee (the truthful fee as nicely). That is thought of the “actual” conversion fee, and that’s the principle distinction with banks, they don’t normally share the true conversion fee with you, as a result of they put the margin on prime of the true fee.

Funding thesis

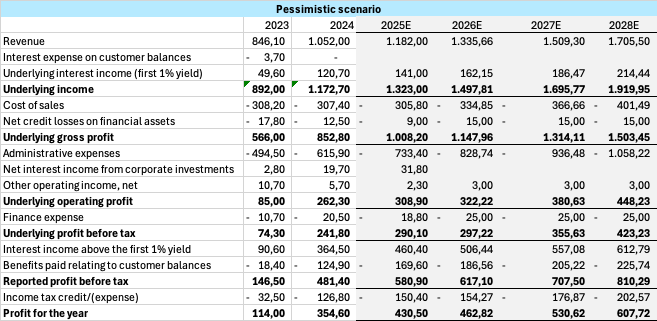

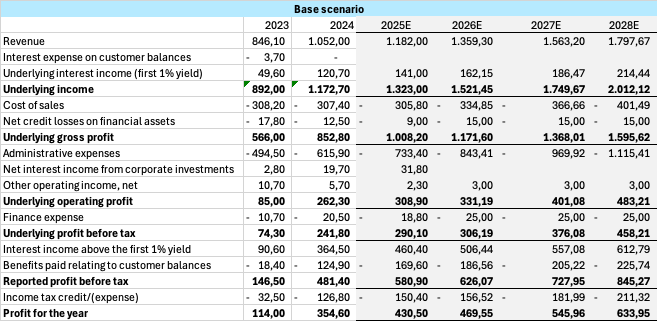

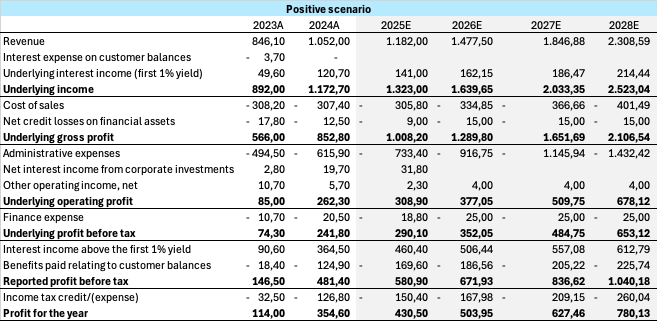

As we’re near the tip of their finish of monetary yr, anticipated in March 2025, I made some estimations of what could possibly be the way forward for the income of the corporate, (once I first purchased a Smart share, my estimations, even the optimistic one had been so low in contrast with immediately outcomes) I needed to renew my eventualities thus far, making new estimations for the interval (2025-2028) for the pessimistic situation I estimated a development of 13% yearly, which is decrease than their very own expectations of a 15-20% development CAGR. For the bottom situation I thought of 15% development of income, excellent within the low vary of their expectations , and for the optimistic situation a really optimistic development of 25%.

Utilizing the mid-point development estimate of the corporate (15%), and being conservative on the curiosity revenue that Smart may have sooner or later, we might see a rise of over 44% web revenue. Thus, utilizing the identical a number of that the corporate trades immediately (25x) we might have a return of over 44% in three years (As a result of the 2025 outcomes are nearly right here and are in base of the final semester outcomes).

If we think about the online money place of the corporate, which stays at 800m, (excluding the client’s held stability), the corporate trades even decrease, which might give us much more upside. Adjusting the online money place, the corporate’s PE ratio is round 24 occasions earnings. We might all the time depart room for multiple-expansion, which given the corporate’s development, return on capital employed, and profitability, is a really probably chance.

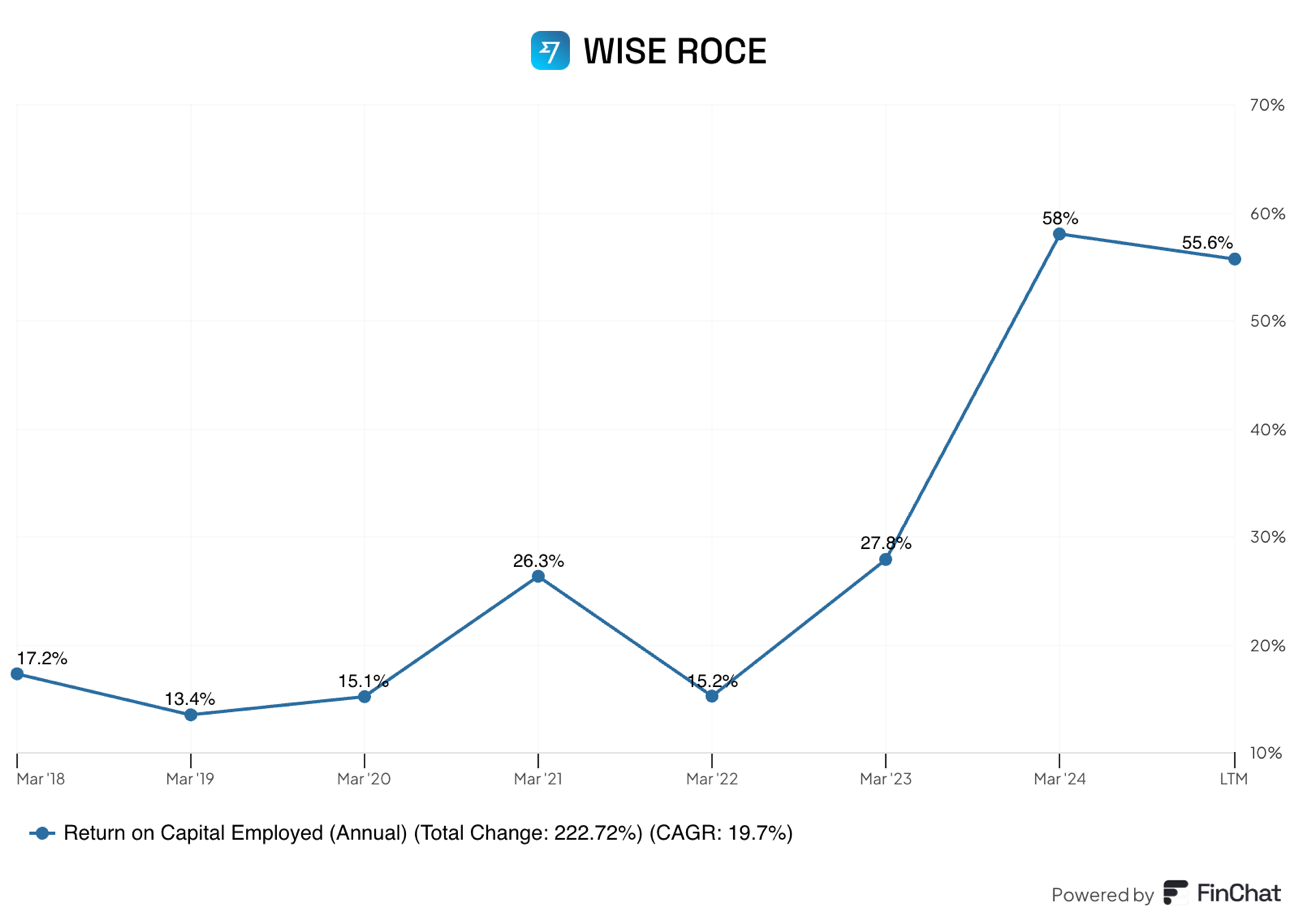

Nevertheless, with the inventory close to all-time highs, is it nonetheless a purchase? With buyer development at 29% YoY and cross-border volumes up 24% to £37.8B, Smart’s fundamentals look robust, with a mean ROCE of 30% within the final 5 years, with clear aggressive benefit by their crimson of partnerships worldwide, rising the variety of prospects +20% quarterly.

However might they maintain the tempo in development in the long run? The TAM (Complete Addressable Market) of the cross-border funds has proven an annual development of three%, Smart’s estimation from their annual report in 2024 are that in 2027 it is going to obtain a complete quantity of £28.5 TRILLION between retail, SMBs (Small and medium enterprise), and enterprises. In 2024 the TAM just for retail was £2 trillion moved yearly. All this info means, that there’s round £28.5 trillion in alternatives for the infrastructure of sensible which is at the moment having lower than the 1% of the market share. However this doesn’t imply that there’s no danger related to the enterprise, right here we’ll discover a number of the important dangers for Smart.

WISE’s RISKS.

Nevertheless, Smart’s plan to beat this, is working along with banks worldwide, providing their prepared to attach infrastructure, and complying with each nation’s totally different rules. Being associate with a considerable quantity of greater than 90 firms from numerous sectors, together with banks, which is a crucial community to assist the bettering of decreasing SWIFT prices, and time. We additionally should think about the size of the corporate, working in over 160 international locations.

The newest information was when Morgan Stanley introduced the settlement with Smart to facilitate the overseas change worldwide capabilities for company prospects, this can be a nice milestone as a result of that is the primary funding financial institution to allow these on sensible, that is the start of many different banks selecting observe this path, as is the case with Normal Chartereds a financial institution in Asia, Africa and the Center East. All of those new relationships imply international presence for Smart.

Fines and compliance that compromise WISE’s mission. Final January the Shopper Monetary Safety Bureau ordered Smart to pay almost $2.5 million for a sequence of unlawful actions, probably the most regarding act was the disclosure of the 6 digit conversion fee, the CFPB mentioned the rule of thumb is between 2 and 4 digit, what make us query if this “Unfair competitors” might probably have an effect on the purchasers within the US, that’s greater than three million of individuals between the 48 states, the District of Columbia, Guam, the U.S. Virgin Islands, and Puerto Rico, within the matter of their mission to make clear transactions. I haven’t discovered any communication from Smart to seek out how they’re anticipating to repair this. Nevertheless a $2.5 milion isn’t a significative quantity contemplating the free money circulate of the corporate.

Forex Volatility. Fluctuations in change charges might have an effect on profitability, however many of the income come from charges in conversion and switch.

The stagnation of the corporate’s development is a sound concern. If the expansion that we expect doesn’t materialize, the valuation and the a number of that the corporate trades at might be harmed. Nevertheless, the loyal base of shoppers (“evangelical prospects” as they name them) creates an unimaginable development in prospects, the TAM confirmed us the probabilities are nonetheless with house to development, as the instance of the doorway of WISE on January to the Mexican market, and the brand new partnership with international banks, makes unlikely the stagnation within the coming three years no less than.

Digital currencies and cryptocurrencies, with globalization of one of these forex, and each time extra international locations acknowledging the makes use of of it, we might see a digital globably accepted, as is the case of the Inthanon-LionRock between Thailand and Hong kong or undertaking Aber between Saudi Arabia and the UAE. So finally you would cease needing to change your cash to totally different currencies, with only one asset you would pay in China, US and in Venezuela. I consider this could possibly be the longer term however in a really perfect world. It will want an excessive amount of cooperation between nations, and that is hardly probably within the coming 20 years no less than.

Credit score danger. To evaluate this subject, the corporate has a really conservative method to speculate their buyer’s stability. As of their newest report, solely 36% of their money place is invested in market funds (3.776m out of 10.479m), whereas the remaining is in present accounts. Relating to their short-term investments, nearly 100% of the cash is invested in Aa and A devices, creating a sturdy and stable stability sheet for the corporate.

Conclusion

Smart was my finest funding in 2024, however in 2025, it’s time to reassess. At 25x earnings and close to all-time highs, is it nonetheless a superb deal? Initially, Revolut’s IPO appeared like another alternative, however after reviewing the restricted knowledge obtainable, its rumored valuation could possibly be seven occasions larger than Smart’s present a number of.

For now, my focus stays on Smart, buying and selling at 25x however rising quickly in each buyer base and international growth. With no debt, a world infrastructure benefit, and a management group aligned with shareholders’ pursuits (CEO and co-founder Kristo Käärmann nonetheless owns 18% of the corporate) Smart stays a compelling long-term funding.

What do you suppose? Will Revolut’s IPO be a game-changer, or is Smart nonetheless the smarter wager?

Sources

Smart annual assertion 2024

Analyst presentation 2024

Revolut annual assertion

https://sensible.com/imaginary-v2/pictures/2bbbb368c98fe4aa7b2aa3e133341520-FY24_Analyst_Presentation_.pdf

https://www.revolut.com/information/revolut_announces_secondary_share_sale_to_provide_employee_liquidity/

https://www.investopedia.com/softbank-backed-revolut-secures-usd45b-valuation-ahead-of-possible-ipo-8696459#:~:textual content=Revolutpercent20haspercent20securedpercent20apercent20$45,intopercent20thepercent20companypercent20inpercent202021.

https://www.theguardian.com/enterprise/article/2024/aug/16/fintech-firm-revolut-valued-employee-share-sale

https://www.statista.com/subjects/11647/cross-border-payments/#topicOverview

https://www.consumerfinance.gov/about-us/newsroom/cfpb-orders-wise-to-pay-25-million-for-illegal-remittance-practices/#:~:textual content=Thepercent20CFPBpercent20ispercent20orderingpercent20Wise,saidpercent20CFPBpercent20Directorpercent20Rohitpercent20Chopra.

This communication is for info and training functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out bearing in mind any specific recipient’s funding targets or monetary scenario, and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product are usually not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}