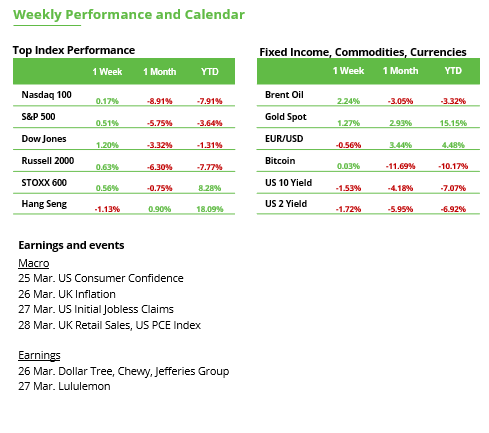

At its March assembly, the Fed saved charges regular at 4.25-4.50%. Don’t pop the champagne but, although. The Fed additionally signalled it’s not declaring victory on inflation: officers nudged their inflation forecasts greater and trimmed progress expectations, citing a “extremely unsure” outlook. Translation? The outlook’s nonetheless foggy, and people inflation-fuelling tariffs aren’t serving to.

What It Means For Your Cash:

Greater-for-longer charges remind us to be selective in shares – deal with firms that may thrive in a moderate-growth, moderate-inflation world.

Banks profit from greater internet curiosity margins (they earn extra on loans vs. what they pay on deposits), and insurers can earn extra from investing premiums.

Shopper staples are likely to have dependable money movement and might go some inflation on to shoppers.

Healthcare demand is non-cyclical — folks want meds and procedures no matter charges. Many healthcare firms have steady money flows and pricing energy.

Not all tech will get punished in a high-rate world. Money-generating companies with robust moats and price management can nonetheless outperform. Cloud, cybersecurity, and AI-infrastructure gamers stay long-term winners.

To keep away from: 1. Excessive-growth, no-profit tech that get hit hardest by greater low cost charges. 2. Actual property (particularly industrial REITs) + greater charges = costlier debt, decrease property values. 3. Extremely leveraged sectors – companies loaded with debt see earnings eaten up by greater curiosity prices.

Earnings Season: Huge Names, Small Surprises

Nike, FedEx, and Accenture all disillusioned—and Wall Road seen.

Nike expects additional income declines, nonetheless untangling final 12 months’s stock overload and seeing weaker demand. Trump’s tariffs on China and Mexico might contribute to a pointy decline in profitability. Nike imports 18% of its Nike-branded footwear from China, which Trump has levied an extra 20% tariffs on.

FedEx is navigating greater prices and a dip in international delivery volumes as companies cool their spending.

Accenture? Down 13% year-to-date after company shoppers hit the cancel button on massive contracts (coupled with DOGE-related cancellations)– a attainable signal that the company spending frenzy of the previous couple of years is easing up.

What’s occurring? If folks aren’t snapping up sneakers like they used to, or shippers like FedEx are seeing fewer packages, it factors to a broader financial cooldown on the horizon. However right here’s the silver lining: a gentle slowdown may be precisely what the Fed (and long-term buyers nervous about overheating) want to chill inflation with no laborious touchdown. And context is essential: all three firms have weathered slowdowns earlier than. Every remains to be a dominant participant in its discipline, with strong long-run prospects. The cautious indicators from Nike, FedEx, and Accenture remind us to regulate the broader financial system’s pulse.

Bottomline: For long-term buyers, dips in confirmed names brought on by non permanent headwinds may even be alternatives. In case you’ve executed your homework and consider in an organization’s long-term story, a 5% drop on an earnings miss may be an opportunity to purchase at a reduction. Simply ensure these short-term points (weak client demand, greater prices, and so forth.) don’t threaten the corporate’s long-term aggressive edge.

PMI Knowledge in Focus: Can Main Indicators Rebuild Investor Confidence?

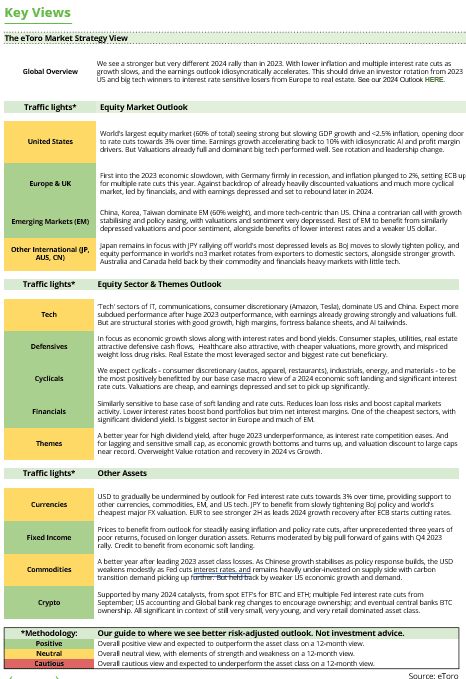

Traders Searching for Course: Market members are dealing with many questions within the present atmosphere – and rightly so. Trump stays the most important uncertainty issue, casting a thick fog over the markets. Many buyers really feel at nighttime, trying to find readability and orientation. Volatility has elevated considerably in latest weeks, notably within the U.S.. In response to the RSI, the S&P 500 futures had been as oversold on the day by day chart as they had been final seen in September 2022, following the latest sell-off. Even the just lately robust European inventory market hasn’t been immune. Whereas the swings have been much less pronounced, the STOXX Europe 600 just lately skilled a 5% dip – a transparent signal that international uncertainty is spreading.

Shifting Market Circumstances: Whereas some buyers see latest worth weaknesses as shopping for alternatives, others consider the correction is much from over. The Fed’s message final week captured the dilemma buyers at present face: uncertainty makes forecasting extraordinarily tough. That doesn’t imply the market is collapsing—however the atmosphere has clearly modified. Volatility is again, and it’s seemingly right here to remain. Slightly than panicking, buyers ought to adapt and get used to the brand new circumstances. In spite of everything, Trump will stay a significant market issue for almost 4 extra years.

PMI Knowledge as a Actuality Examine: Main indicators aren’t the holy grail, however they provide a helpful glimpse into what’s forward. On Monday, the March PMI knowledge for Europe and the U.S. might be launched and will function a well timed actuality examine for buyers. Within the U.S., the image has shifted in latest months (see chart under). The manufacturing sector (52.7) has managed to get well from its downturn, whereas the providers sector (51.0) continues to point out indicators of weak spot. The same development could be seen in Europe, although with a key distinction: manufacturing stays in recession territory (47.6), whereas the providers PMI is hovering nearer to the impartial 50 mark (50.6). Traders ought to watch intently for brand spanking new momentum or vital deviations from expectations. The primary focus stays on inflation dangers, notably these linked to rising tariffs.

Federal Council Approves Germany’s Monetary Package deal: The deliberate €1 trillion in new debt might be financed by way of varied channels. Infrastructure and local weather investments might be funded through a particular fund, whereas protection, safety, and help for Ukraine might be lined by a relaxed debt brake. The muted market response within the DAX, euro, and German authorities bonds means that the elevated public spending was largely priced in. One factor is obvious: curiosity prices will rise and put long-term strain on the federal price range. A powerful financial restoration might be important to maintain the debt manageable—for now, markets stay hopeful that Germany’s financial system will rebound considerably within the coming years.

Bottomline: Traders ought to take the Trump issue severely, however not panic. The secret is to remain calm and suppose long-term. Rising volatility additionally presents new alternatives—those that stay versatile can profit. Consideration also needs to be paid to the differing dynamics between the U.S. and Europe. The upcoming PMI knowledge might be an vital indicator. Germany’s monetary package deal could present a short-term increase, however what actually issues is whether or not the investments are focused and successfully applied to help sustainable progress.

This communication is for data and training functions solely and shouldn’t be taken as funding recommendation, a private advice, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out making an allowance for any specific recipient’s funding targets or monetary state of affairs and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product usually are not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}