Markets confronted a whirlwind of tariffs, CEO warnings, and Huge Tech actuality checks final week. Coverage shifts and earnings set the stage for what’s subsequent – and all eyes are actually on the tech giants able to report. Right here’s what traders must know heading right into a essential stretch.

Tariff Pressures Eased After CEO Warnings:

After market turmoil, falling polling numbers, and warnings from the CEOs of Walmart, Goal, and Residence Depot about larger costs and empty cabinets resulting from tariffs, the US has made a collection of concessions that display there’s now an effort to show down the temperature on tariffs. Buyers are adjusting portfolios, with client, retail, and industrial sectors more likely to profit if commerce tensions keep contained. Whereas a full US- China deal will not be completed, the shift lowered the temperature for now- a reminder that coverage danger stays a swing issue for markets worldwide.

Mega-Cap Tech’s Actuality Examine: The once-invincible Magnificent 7 tech giants are coming again to earth. Their earnings progress remains to be outpacing the remainder of the S&P, however by a far slimmer margin heading into 2025-26. AI & Software program – Silver Lining: One clear shiny spot amid the uncertainty is the continued growth in AI and enterprise software program. From cloud computing to generative AI, tech leaders are doubling down on innovation to drive effectivity and new income streams. This week’s Huge Tech earnings are anticipated to hammer this residence, which may showcase AI prowess and resilient software program demand. For traders, the message is that long-term tech themes (AI, cloud) stay intact – even when the macro winds blow chilly within the brief time period.

Huge Tech Earnings Bonanza Upcoming: This week brings a tech earnings bonanza that would set the market tone. 4 of the 5 largest US tech companies report this week: Meta and Microsoft on April 30, and Apple and Amazon on Could 1. All eyes will likely be on their outcomes and steering – particularly any commentary on cloud spending, digital advertisements, and AI initiatives. Buyers will likely be on the lookout for affirmation that innovation and price self-discipline can counterbalance any financial softness.

Key focus areas:

Cloud Spending: AWS, Azure, and Google Cloud outcomes will present how IT budgets are evolving in a extra cautious economic system.

AI Commercialization: Progress on AI product rollouts and monetization will likely be essential for market sentiment.

Client Demand Alerts: Apple’s iPhone and providers progress will likely be a serious learn on discretionary spending resilience.

Promoting Traits: Meta and Google will present perception into small and mid-sized enterprise advertising budgets – a number one indicator for broader financial well being.

High 3 Themes to Look ahead to:

Tariff De-escalation = Retail and Client Aid: Commerce concessions might ease stress on provide chains and margins.

Software program and AI = Relative Energy:Software program and AI adoption developments are robust, even in opposition to macro headwinds.

Huge Tech Earnings = Market Catalyst: Ahead steering will form danger urge for food throughout sectors, not simply in expertise.

Between tariff coverage and financial knowledge – traders want robust nerves

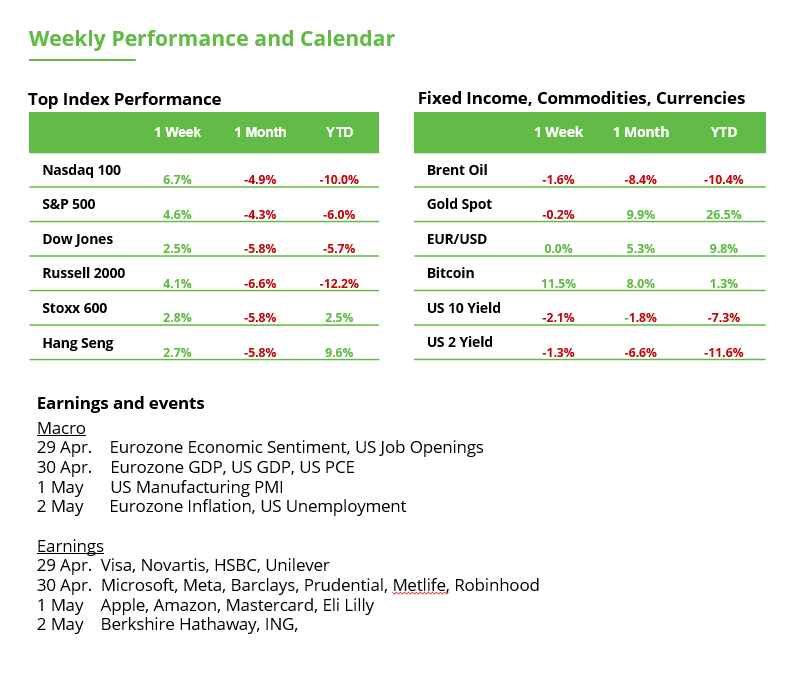

The calendar is full of necessary updates: Current weeks have clearly proven how delicate markets are to new headlines, which may result in sharp short-term strikes. In unsure occasions, macro knowledge and earnings season present real-world insights past hypothesis.

The Fed’s most well-liked inflation gauge: The Core PCE Worth Index stays clearly above the central financial institution’s 2% goal, at present sitting at 2.8%. The important thing will likely be whether or not the March knowledge, due Wednesday, present a significant decline. The ISM Manufacturing PMI, due Thursday, is predicted to fall from 49.0 to 47.9. That might sign weakening industrial exercise and will assist expectations for fee cuts – supplied inflation continues to ease and Friday’s labor market knowledge additionally are available in weak.

Germany stays Europe’s weak spot: Inflation and GDP knowledge from Europe on Wednesday will notably spotlight Germany. The area’s largest economic system has been in recession for 2 years. The German authorities expects stagnation at greatest in 2025. And but, the DAX retains reaching new document highs. The rationale: DAX-listed firms generate 82% of their income overseas. The inventory market due to this fact displays world progress, not the home German economic system.

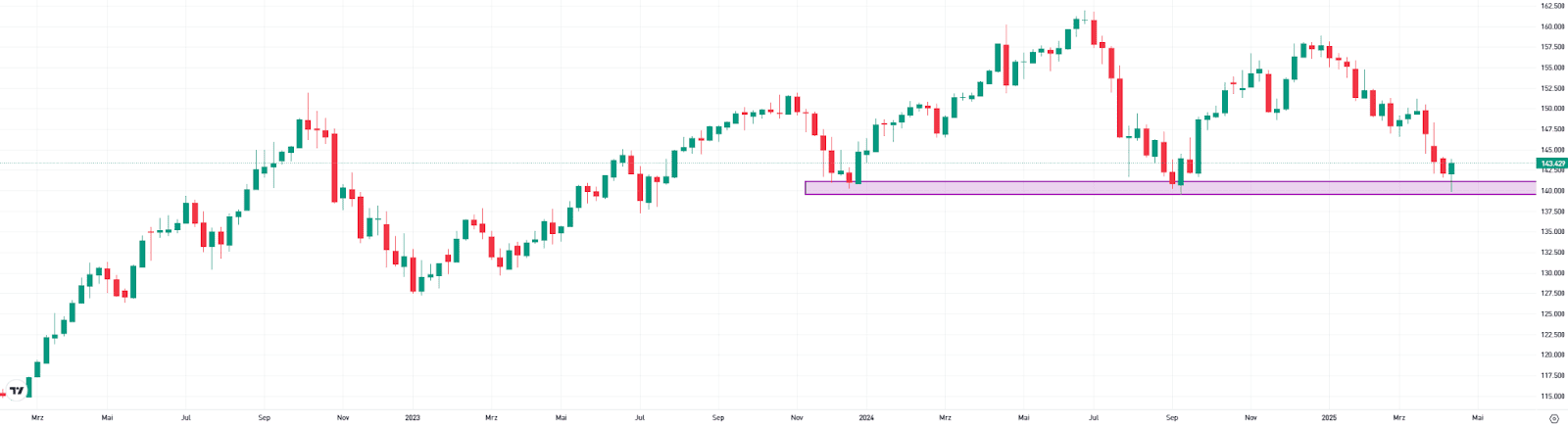

Japan: Not like most different central banks, the Financial institution of Japan is at present in a rate-hiking cycle. Nonetheless, it’s anticipated to carry charges regular on Thursday. Merchants will likely be watching carefully to see whether or not additional fee hikes is likely to be delayed or whether or not there’s imminent want for motion. A hawkish tone would doubtless assist the yen additional. The USD/JPY pair has fallen by 8% over the previous three months and examined long-term assist round 140 final week (see chart).

Bottomline: Given the flood of knowledge from the US and Europe, there could possibly be loads of short-term buying and selling alternatives in EUR/USD. The pair has been buying and selling in a slender vary between 1.13 and 1.14 in latest days. Rate of interest-sensitive sectors resembling expertise, financials, and actual property might react notably strongly to adjustments in fee expectations. For USD/JPY, we could quickly see whether or not a long-term pattern shift is underway.

USD/JPY

This communication is for info and training functions solely and shouldn’t be taken as funding recommendation, a private advice, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out considering any explicit recipient’s funding aims or monetary scenario and has not been ready in accordance with the authorized and regulatory necessities to advertise impartial analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product are usually not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}