The Every day Breakdown takes a more in-depth take a look at Palo Alto Networks as shares have misplaced one-third of their worth from the latest highs.

Earlier than we dive in, let’s be sure to’re set to obtain The Every day Breakdown every morning. To maintain getting our day by day insights, all that you must do is log in to your eToro account.

Deep Dive

We’ve spent loads of time on the AI-driven selloff in software program — and it’s now spilling into areas like bank card networks, ranking companies, and cybersecurity. The irony is that many bulls view AI as a catalyst for cybersecurity, not a risk. That’s to not say AI can’t introduce new dangers, nevertheless it’s a reminder that Wall Avenue will be short-term and emotional. With that in thoughts, a contemporary take a look at the charts pushed us to take a deeper dive into Palo Alto Networks.

Palo Alto Networks offers cybersecurity services globally, spanning next-gen firewalls, cloud safety, safe entry, and risk prevention/detection. It additionally sells subscriptions for risk intelligence, malware safety, and knowledge loss prevention, alongside skilled providers, coaching, and help.

Usually considered as a blue-chip within the house, Palo Alto could not supply the identical top-line development as friends like CrowdStrike, Zscaler, or Fortinet, nevertheless it tends to deliver stronger financials. The corporate is solidly worthwhile, generates constant free money circulation, and has used that power to take a position for the long run. Most notably, it not too long ago acquired CyberArk — a deal Palo Alto framed as a solution to capitalize on key AI-driven developments.

Future Progress Projections

The corporate’s fiscal 12 months ends in July (which means fiscal 2026 ends on July 31, 2026). In accordance with Bloomberg, analysts venture the next:

Earnings Progress: 10.8% in 2026, 7.8% in 2027, and 16.8% in 2028

Income Progress: 22.2% in 2026, 19.8% in 2027, and 13.7% in 2028

Free Money Circulate Progress: 17.4% in 2026, 23.2% in 2027, and 14.4% in 2028

Analysts at the moment have a consensus worth goal of ~$215 on PANW inventory, implying about 44% upside to in the present day’s inventory worth.

Need to obtain these insights straight to your inbox?

Enroll right here

Diving Deeper — Valuation

With cybersecurity shares typically richly valued, that alone generally is a hurdle for some traders. Whereas Palo Alto doesn’t command the nosebleed multiples of some friends, it nonetheless trades at a premium to many extra conventional industries.

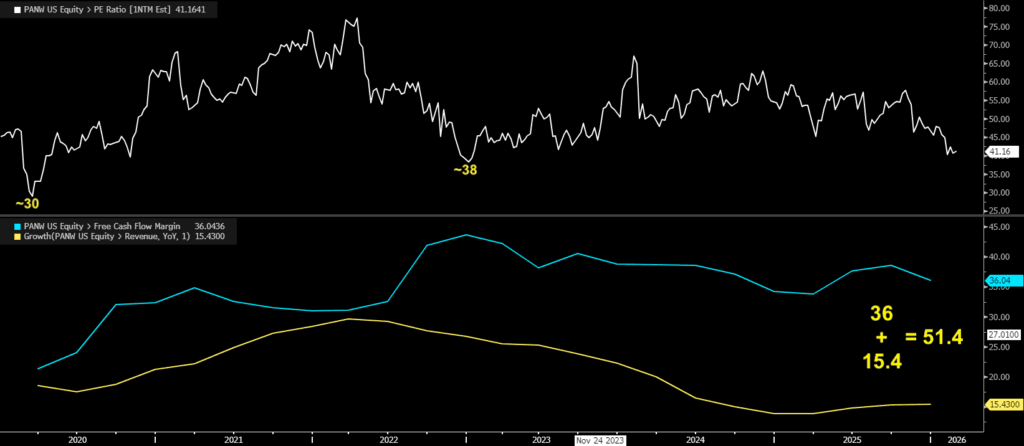

The highest chart exhibits PANW’s ahead P/E ratio, which has fallen to its lowest stage in a number of years. Throughout the 2022 bear market, the a number of bottomed close to 38x, whereas the COVID-19 selloff in 2020 pushed it all the way down to roughly 30x.

The underside chart highlights free money circulation margin and income development. The “Rule of 40” — a key SaaS (Software program as a Service) metric — says an organization’s income development price plus its free money circulation margin ought to be at the very least 40%. Utilized by traders to judge firm well being, this system balances fast development with profitability. By that measure, Palo Alto at the moment scores 51.4.

Dangers

There are a number of dangers for Palo Alto — and a few have been on show not too long ago. The largest near-term overhang is AI-disruption concern; even when it proves overblown, the notion alone can stress sentiment and the a number of. Past that, a broader tech selloff may weigh on shares, and intense competitors may gradual development.

The Backside Line

For some traders, the uncertainty is simply too excessive or the valuation nonetheless isn’t compelling. For others, the latest ~30% pullback could appear like a lovely entry level to start out constructing a place.

Disclaimer:

Please observe that as a result of market volatility, a few of the costs could have already been reached and situations performed out.

{kind=link}