The article beneath is an excerpt from a latest version of Bitcoin Journal PRO, Bitcoin Journal’s premium markets e-newsletter. To be among the many first to obtain these insights and different on-chain bitcoin market evaluation straight to your inbox, subscribe now.

Aug. 17, marked the return of the much-awaited and infamous bitcoin volatility. After a number of months of consolidating across the $30,000 stage with traditionally low realized and implied volatility within the bitcoin market, the worth lastly woke up, bringing concerning the greatest liquidation occasion bitcoin has seen in years. Opposite to some opinions by reporters and analysts, the bitcoin crash was not triggered by rumors of SpaceX promoting bitcoin or some other news-based occasion. Not like a inventory, bitcoin doesn’t have earnings calls or unhealthy information about future prospects that may tank the worth or dampen the community’s fundamentals.

Sure, occasions such because the approval (or dismissal) of a spot bitcoin ETF may change the market’s anticipated flows, however this was not the case throughout Thursday’s value crash. As a substitute, the market transfer was , old school by-product liquidation, a easy occasion of extra sellers than consumers, with the decision being a price-clearing mechanism to the draw back.

In earlier points, we wrote about bitcoin’s traditionally low realized and implied volatility, noting that such intervals result in massive bounces in volatility and explosive breakouts in both route. Clearly, the latest decision was to the draw back, but it surely may result in a brand new regime in bitcoin, a minimum of quickly, because the market makes an attempt to discover a new equilibrium within the short-to-intermediate-term.

Since this was largely a by-product phenomenon, let’s discover a number of the mechanics behind this large transfer. In bitcoin, whereas the choices market is much less developed and mature in comparison with equities, there was development relative to the futures market in recent times, and development in each markets in comparison with the spot market since 2017. It is essential to notice that the proliferation of a futures/derivatives market isn’t essentially good or unhealthy. With an equal quantity of lengthy and quick positions, the web impression over a protracted sufficient time-frame is impartial. Nonetheless, within the shorter-to-medium time period, a creating derivatives market on high of the spot market can result in massive dislocations that lead to sudden volatility, with the market buying and selling aggressively in a single route or the opposite to resolve the imbalance.

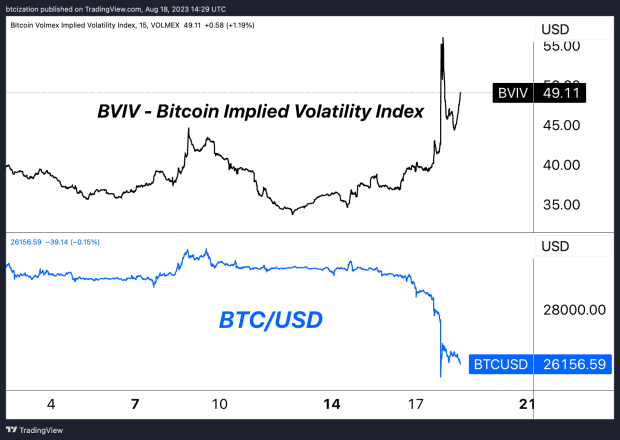

When observing a interval of downtrending implied volatility derived from pricing within the choices market, we are able to see what merchants and speculators assume an asset’s future volatility will appear like. Quick volatility methods, whether or not easy or complicated, are primarily bets on decrease and/or stagnant volatility sooner or later. On this case, observing the pattern in bitcoin’s implied volatility by the Volmex Bitcoin Implied Volatility Index (BVIV), we are able to conclude that promoting or shorting volatility turned a well-liked commerce over the summer season months, successfully proscribing the bitcoin market to a given value vary.

When market contributors promote volatility by choices, market makers reply by adjusting their hedges within the underlying asset, making a stabilizing “pinning” impact close to sure value ranges the place there’s substantial open curiosity. To take care of a impartial place, market makers dynamically purchase or promote the underlying asset in response to cost actions of choices, reinforcing the pinning impact. This equilibrium, nevertheless, could be shattered by sudden occasions or shifts in sentiment, inflicting market makers to quickly re-hedge. This results in a sudden and important value and volatility motion, reflecting the fragile and interconnected nature of choices buying and selling, market making and asset dynamics. That is exactly what occurred.

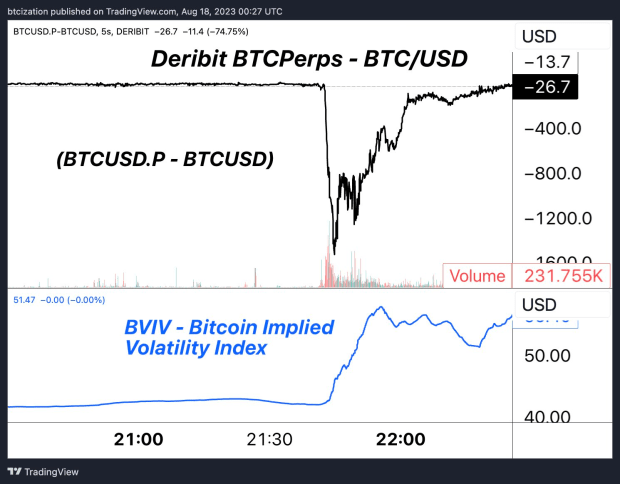

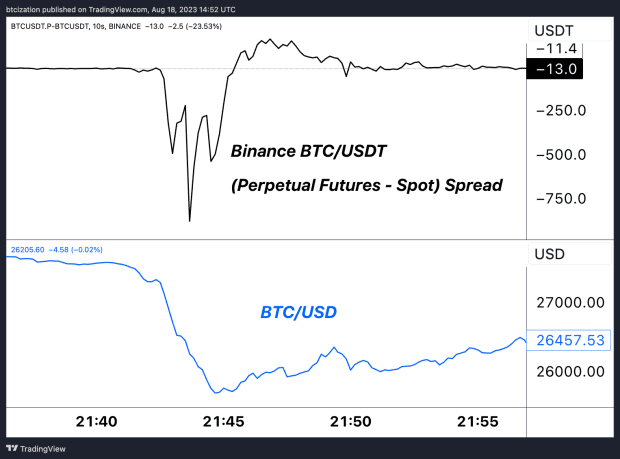

Taking a look at Deribit, the first choices market for bitcoin/crypto, the unfold between their perpetual swaps market and the spot bitcoin market widened massively as implied volatility expanded. Contributors who had been getting cash by shorting or promoting volatility have been caught unexpectedly, main to an enormous dislocation and liquidation occasion.

All that being stated, this wasn’t simply an options-driven occasion. There was rising leverage within the futures market as effectively. Spot market volumes at multi-year lows mixed with rising by-product volumes and open curiosity along with volatility close to multi-year lows, was akin to lighting a match close to a pile of dynamite and ready for ignition. Alas, a spark was lit.

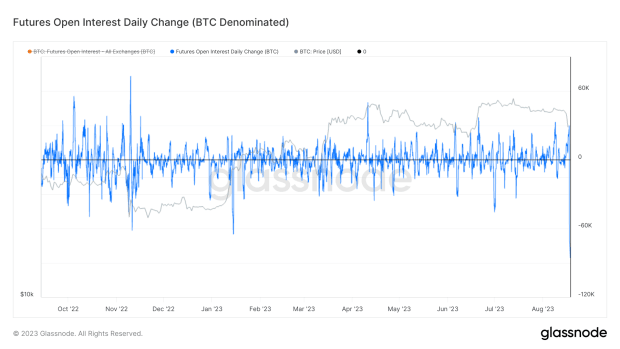

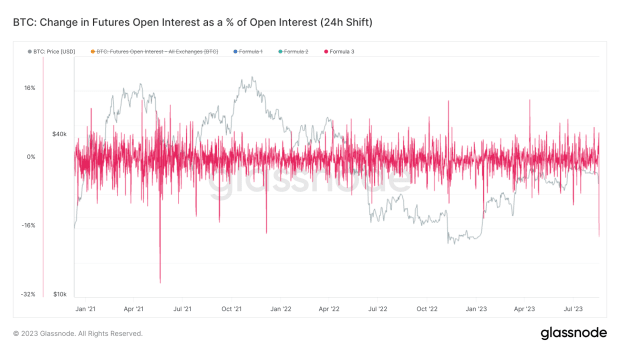

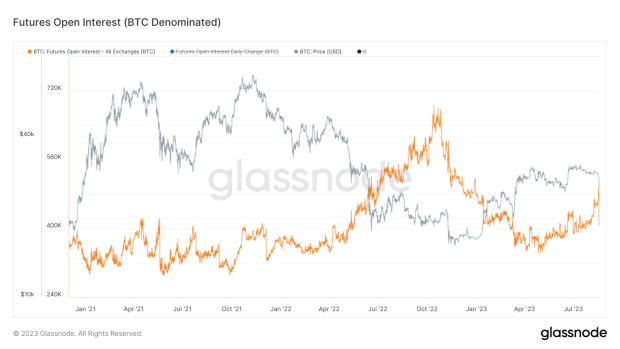

In bitcoin-denominated phrases, the day by day change in open curiosity was bigger than the collapse of FTX, with 89,000 BTC much less open curiosity than 24 hours prior.

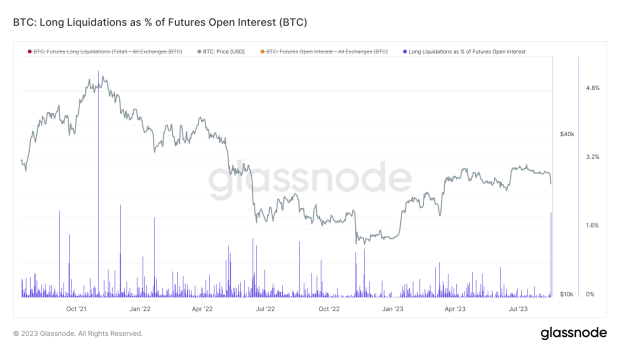

As a share of the futures market, with a 24-hour interval to match up the timelines, the transfer was equal to 18% getting worn out or closing, one thing that hasn’t been seen since December 2021.

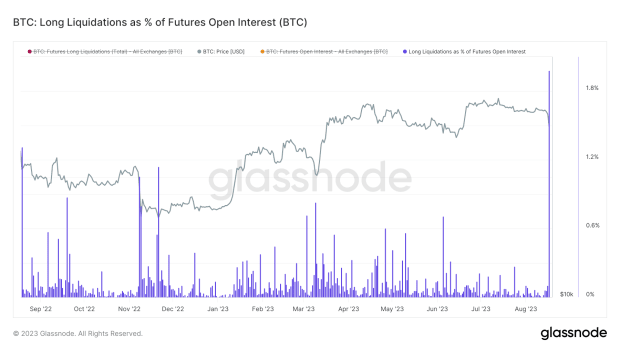

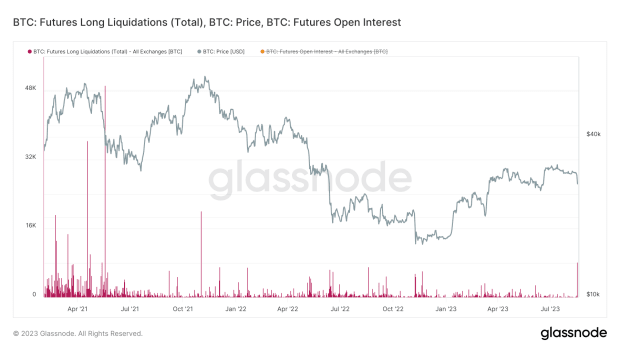

Trying solely at open curiosity liquidations, Glassnode finds 8,141 BTC getting liquidated throughout Thursday’s transfer, the biggest since November 2021, and roughly 2% of open curiosity that forcefully received liquidated or margin referred to as.

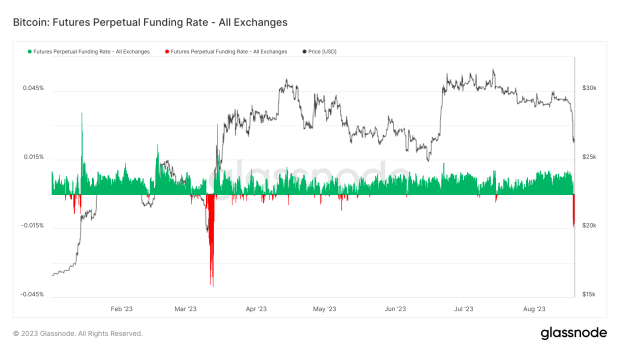

Looking at funding charges — the variable rate of interest paid between lengthy and quick positions within the perpetual futures market to incentivize merchants to maintain the contract value near the spot market — funding fell to its lowest stage because the March banking disaster when Silicon Valley Financial institution failed and USDC depegged. This exhibits simply how massive the dislocation within the derivatives market was relative to the spot market. Whereas it’s too early to attract conclusions a couple of important quick bias available in the market as a result of unfavorable funding fee, we are going to monitor the market over the approaching days and weeks. A interval of sustained unfavorable funding with rising open curiosity may result in situations conducive to a brief squeeze, though this has but to develop.

Closing Notice:

In conclusion, whereas Thursday’s transfer was the biggest bout of volatility seen all 12 months and the biggest bitcoin derivative-driven phenomenon in fairly a while, it’s typical of intervals of extraordinarily low realized and implied volatility in any market, not to mention that of a notoriously risky and unpredictable digital asset nonetheless in its monetization section. Within the quick time period, we now count on a pickup in volatility and better uncertainty as the worth tries to discover a new equilibrium level, with loads of information forward relating to potential bitcoin spot ETF approvals heading into 2024.

That concludes the excerpt from a latest version of Bitcoin Journal PRO. Subscribe now to obtain PRO articles straight in your inbox.

{kind=link}