Key Takeaways:

Latam remittances have reached an estimated $174B, though the expansion is just not following the US-Mexico route. Stablecoins have since overturned crypto use within the space and at the moment are principally used as a approach to save cash, relatively than a type of fee. Nearly all of fintechs give attention to the mistaken customers/corridors and overlook giant underserved markets.

Stablecoins are quietly reshaping cross-border funds in Latin America, however most fintech methods are nonetheless misaligned. New insights from Bybit’s CMO Claudia Wang present the true drivers behind a fast-evolving $174 billion market.

https://t.co/Thxx7UTWRO

— Claudia (@0x_claudia) Could 3, 2026

Learn Extra: $315B Stablecoin Market Faces BIS Warning as Greenback Tokens Threaten Finance Stability

LATAM Flows Shift Away From Mexico

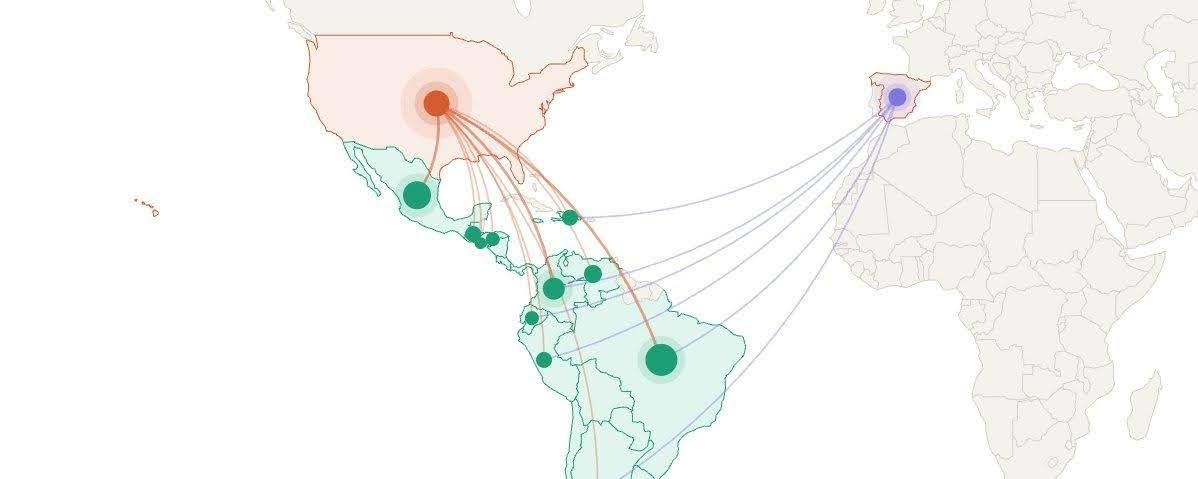

Remittances into Latin America reached a file ~$174 billion in 2025. However progress is now not centered on Mexico.

Mexico skilled the autumn of 4.5% to $61.8 billion. Central American nations within the meantime shot up with over decade growths in Guatemala, Honduras and El Salvador.

This shift displays altering migration patterns. Migrants from Central America are sending cash house quicker and in bigger quantities, usually reacting to coverage strain within the U.S.

Most fintechs nonetheless give attention to the US – Mexico hall. That’s a mistake. Smaller routes, particularly non-U.S. corridors, stay underserved and face much less competitors.

Stablecoins Are Held, Not Simply Despatched

Customers Need {Dollars}, Not Transactions

Stablecoins now account for round 40% of all crypto purchases throughout LATAM, overtaking Bitcoin.

However the important thing perception is behavioral. Customers are usually not utilizing stablecoins simply to switch cash. In some nations comparable to Argentina, stablecoins management greater than 70% of the crypto purchases. This is a sign of excessive demand for greenback publicity as there may be inflation and capital controls.

The Actual Remittance Consumer Is Not Crypto-Native

Fintech merchandise usually goal younger, tech-savvy customers. That’s not who drives remittances. The standard sender is 40–60 years previous, sending $100–$600 month-to-month to the household. Greater than 80% of the cash is spent on primary wants comparable to meals and shelter.

This demographic prefers featureless options over options. When the method of sending cash appears tough, they won’t use the commodity. Cell-first design, the help of an area language, and fast affirmation is extra vital than superior crypto instruments.

Learn Extra: Visa Provides 5 Blockchains to $7B Stablecoin Community, 50% Surge Fuels Adoption

Prices and Competitors Are Shifting Quick

Typical remittance service suppliers proceed to cost on the order of 5%-6% per transaction. On the similar time, market share is shifting.

Different legacy gamers within the telecommunication market comparable to Western Union are behind the occasions, in contrast to digital platforms. There may be additionally a rise within the variety of crypto-native firms, notably within the areas the place typical companies are both too pricey or restrictive.

Regulation and Technique Divide the Area

LATAM is just not a single market. Each nation possesses its personal guidelines and infrastructure in addition to consumer conduct. Argentina and Colombia are simpler to enter. Brazil and Mexico are greater and more difficult as regulation is extra strict.

One other dimension, which was added not too long ago within the U.S. coverage, is the 1% tax on the money remittance. That is driving customers in the direction of on-line and crypto-based remits. Corporations capable of modify to those variations and combine each native fee rails and mixture of stablecoin liquidity are in a greater place to reply to long-term demand.

{kind=link}